Private investors looked into business centers

Experts have recorded a record demand for Moscow offices over the past 10 years. This trend has an explanation — against the backdrop of the current economic situation, company executives, institutional and private investors are insuring themselves and buying up “protective” assets — office blocks and business centers. Despite the growing cost of commercial real estate construction, the volume of investments in the segment will remain at a high level until the end of this year.

According to preliminary results for the first half of 2024, the total supply of office space in Moscow amounted to 20.5 million sq. m. m., — reported «MK» Head of the office space department at IBC Real Estate Ekaterina Belova. Totally in January – In June, 310 thousand square meters were put into operation. m.

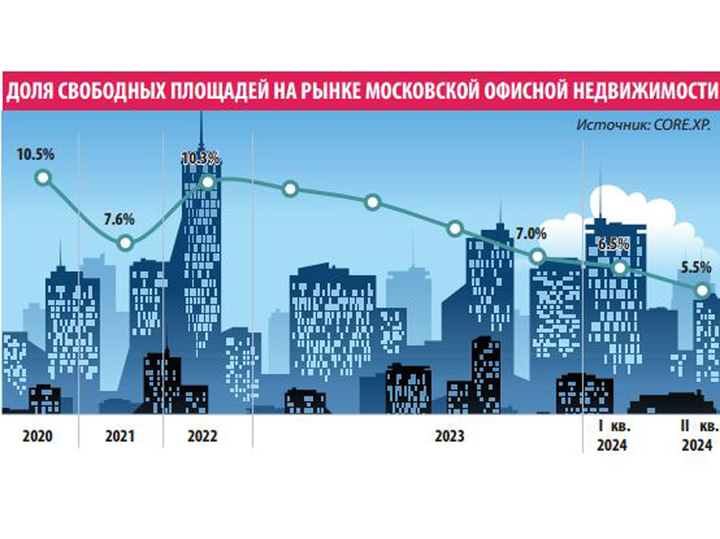

In June, the share of vacant space in the office market as a whole amounted to 6.7%, which is 1.4 percentage points higher. lower than the result at the end of 2023. For Prime class buildings, the vacancy rate was 8%, for class A — 7%, for class B+ the share of free space was fixed at 5%. Thus, for all classes there is a decrease in the share of vacant space compared to 2023. The indicator for class A offices has adjusted most significantly — from 10.4% at the end of 2023 to 7%, decreasing by 3.4 percentage points

Over the past six months, average rates have not changed much (22.6 thousand . rub./sq. m per year (without VAT and NUTS). For class A the figure was 26.4 thousand rubles/sq. m per year (without VAT and NUTS), for class B+ 21.5 thousand rubles/sq. m per year (excluding VAT and NUTS), — noted the expert.

In the face of a shortage of available space, tenants are forced to speed up the process of concluding transactions or take a wait-and-see approach, — explained «MK» Head of the office real estate department CORE.XP Irina Khoroshilova. According to her, the upward trend in the share of purchase and sale transactions continues. This is especially noticeable in the segment of retail transactions up to 1 thousand sq. m. m. This is explained by two factors. Firstly, the demand for offices as a reliable investment tool. Secondly, the growth of the supply available for purchase.

According to preliminary data, the volume of new lease and purchase and sale transactions in the first half of 2024 may reach 700-800 thousand square meters. m. This is comparable to the record first half of 2023, when 870 thousand sq. m. were concluded. m of new deals.

The tenant's portrait has hardly changed. In the first half of the year, state corporations continue to be the most active and government agencies. Their share accounted for about 21% of the total volume of transactions. Representatives of IT and retail are also visible (14% share in demand). In addition, analysts note today increased interest to transactions with companies from the industry, construction and real estate.

According to Irek Allayarov, managing partner of the SOK smart office network, coworking popular among small businesses, individual entrepreneurs and self-employed people. For them, this is the most convenient format, when for little money they get not only a workplace, but also a community, training, the opportunity to collaborate, sell their products, as they say, without leaving the cash register.

But there have been changes in the structure of buyers. Wealthy individuals have been added to institutional investors and large companies this year. Many of them, in anticipation of the end of the state program of preferential mortgages for residential new buildings, reoriented themselves to office buildings. Now achievable levels of profitability from leasing space are 8-10% with a payback period of 10-12 years. Therefore, investors often buy lots in slices, which are increasingly considered as a protective asset for saving money.

Most offices are rented in the area between the Third Transport Ring and the Moscow Ring Road — this is almost half of the total vacancy in Moscow. According to Belova, Most of the expensive options are located in the Moscow City business district – the weighted average rental rate for class A offices there is 46.4 thousand rubles/sq. m. m per year (excluding VAT and NUT), which is almost 2 times the average for the capital.

The largest volume of budget free options is located outside the Moscow Ring Road — the weighted average rental rate in this location is 13.2 thousand rubles/sq.m. m per year (excluding VAT and NUT).

In the most popular locations (Big City, Belorussko-Savelovsky district) the cost of purchasing such offices averages 400 thousand rubles per sq. m. m. “Beyond the Moscow Ring Road there are more budget proposals. Purchase price outside the ring per sq. m office is half as low, — noted Irina Khoroshilova.

This year, the trend toward decentralization of the office segment is gaining momentum. Increasingly, in new residential complexes, developers provide for this format at the design stage.

Despite the increased cost of commercial real estate construction, investor activity remains at a high level. “The great demand for flexible spaces influences the interest of investors in this type of real estate, and also attracts the attention of property owners,” — noted «MK» Allayarov. Due to the great specificity of work in this market, the latter are interested in cooperation with operators. Solid demand, service requirements, and the growing cost of building materials lead to new models of interaction appearing on the market. One of the most popular today — sharing of capital expenses (CapEx) with the operator. Moreover, the popularity of service offices is observed both in capitals and in regions.

According to his forecast, the supply and demand ratio in the flexible office space format is unlikely to change in the near future. New sites that open are immediately filled with tenants. There are many examples where sites do not even have time to appear on the market, since they are quickly rented out.

“The volume of vacant space on the market continues to decrease in all classes against the backdrop of stable demand and virtually no new input,” Khoroshilova is sure. According to her estimates, by the end of the first half of 2024, the share of vacant space will decrease to 5.3-5.5%.

By the end of 2024, 760 thousand square meters are expected to be commissioned. m. This figure is more than 2.5 times higher than the result of 2023, — Belova reported. She expects the total transaction volume for 2024 to be 1.7 million square meters. m. This is 15% lower than the record 2 million sq. m. m in 2023. The weighted average rental rate for the market as a whole based on the results of 2024 is predicted by her at the level of 24 thousand rubles/sq. m. m per year (excluding VAT and NUT), which will be 6% higher than the figure at the end of last year.

«In the next four years, the volume of new office real estate commissioned in Moscow may amount to about 2.7 million sq. m. . m, which is comparable to the volume of construction over the past eight years,” — said the head of the department for work with real estate clients of Sberbank; Arsen Ohanjanyan. In his opinion, additional volumes of commissioning will be generated by housing developers as part of the program for the development of places of employment (MPT). By 2029, under agreements with the city administration, it is planned to build office and business centers with a total area of over 1.2 million square meters. m. The authorities expect to employ about 97 thousand people in these facilities.